A detailed look at Australia’s wine supply and demand

Market bulletin | Issue 80

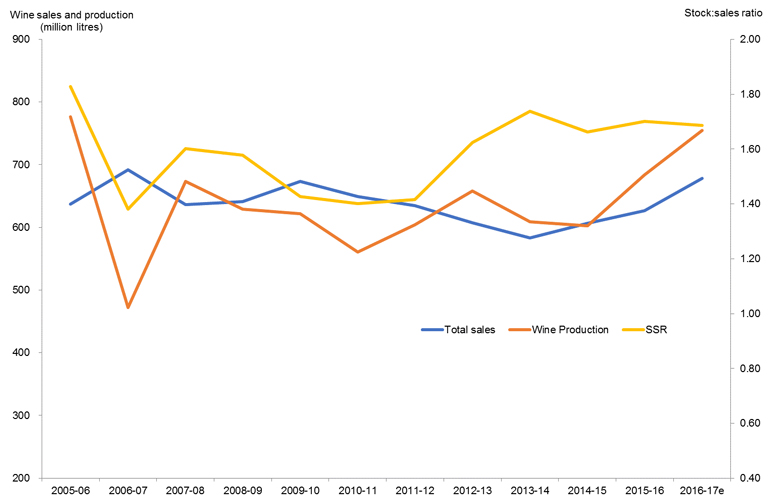

Australian wine production has outstripped sales over the last two years, which has seen Australian wine stocks build.

In 2016–17, it is estimated that 1.35 billion litres of Australian wine were produced, while Australian wine sales totalled 1.27 billion litres. This led to stocks of Australian wine to increase to an estimated 1.84 billion litres. The estimated stock-to-sales ratio (SSR) is now 1.45, which is outside the ideal range of 1.3–1.4. While production and stocks have been increasing to support growth in demand – particularly in China – the SSR provides an early warning sign about stock levels.

Figure 1: Australian wine stocks, production and sales over time

The increase in Australian wine stocks has come from both red and white wine, but reds contributed a greater proportion of the estimated increase.

Figure 2 illustrates that the white wine SSR is outside the ideal range for whites of 1.0 to 1.1 but, with a reduction in white wine production in 2016–17, the SSR has stabilised.

Figure 2: Australian white wine production, sales and SSR over time

Source: Wine Australia

Figure 3 shows the SSR for red wine has been outside the ideal range for reds of 1.5–1.6 for the last four years. While sales of Australian red wines have increased over the last three years, production of red wine over the last two years significantly exceeded sales, leading to an increase in red wine stocks.

Figure 3: Australian red wine production, sales and SSR over time

Source: Wine Australia

Almost 70 per cent of Australian red wine sales are in export markets and hence these sales are vital in assessing the supply and demand situation. In 2016–17, exports of Australian red wine increased by 10 per cent, after growing by 4 per cent in 2015–16 and 5 per cent in 2014–15.

Much of the volume of Australian red wine exports (84 per cent) is at below $5 per litre and exports in this price segment grew 9 per cent in 2016–17. In comparison, exports above $5 per litre increased at a faster rate, up by 12 per cent.

By volume, the United Kingdom (UK) is the biggest export destination for Australian red wine. Exports to the UK declined by 9 per cent to 123 million litres in 2016–17. The decline in exports to the UK was more than offset by increases in exports to mainland China (up 59 per cent to 109 million litres), the United States (up 9 per cent to 81 million litres) and Germany (up 13 per cent to 20 million litres).

If red wine exports continue to grow at the recent strong rates, then stocks should be drawn down and the SSR would revert to more reasonable levels. Furthermore, the expected historically low harvests in France, Italy and Spain, as well as smaller vintages in Argentina and Chile, may provide a further boost to the demand for Australian red wine.

Recent bulk wine prices from Ciatti Global Wine and Grape Brokers show that Australian bulk prices for key Australian reds are already firming (see figure 4).

Figure 4: Bulk wine prices for Australian red wine varieties

Source: Ciatti Global Wine and Grape Brokers

For a more detailed analysis of the Australian wine sector in a global context, see the Australian Wine Sector State of Play Sept 2017 (levy-payers only).

Wine Australia will provide an update on the Australian supply and demand situation when the results of the Production, Sales and Inventory Survey 2017 are released later this year. The International Organisation of Vine and Wine (OIV) will release the first 2017 estimations of the global wine production on 24 October, which will provide an update about the supply situation in Australia’s major competitors.