A drop in wine production around Australia was not enough to offset a reduction in total sales, leading to an increase in the national wine inventory for the second consecutive year, according to Wine Australia’s Production, Sales and Inventory Report 2022 released today.

Based on responses to the Production, Sales and Inventory Survey[1], total Australian wine production in 2021–22 is estimated to be just over 1.3 billion litres, or 145 million 9-litre case equivalents. This was a 12 per cent reduction – the equivalent of approximately 190 million litres (21 million cases) – compared with the record wine production in 2021, but was 4 per cent above the 10-year average of 1.25 billion litres.

Red wine production is reported to have decreased to an estimated 713 million litres – 16 per cent below last year but 6 per cent above the 10-year average. White wine production[2] was estimated to be 594 million litres, 6 per cent lower than in 2021 but still 2 per cent above the 10-year average (see Figure 1).

Figure 1: Australian wine production by colour (historical)

The smaller relative decrease in white wine production compared with reds led to white wine’s share of production increasing from 42 per cent in 2020–21 to 45 per cent in 2021–22.

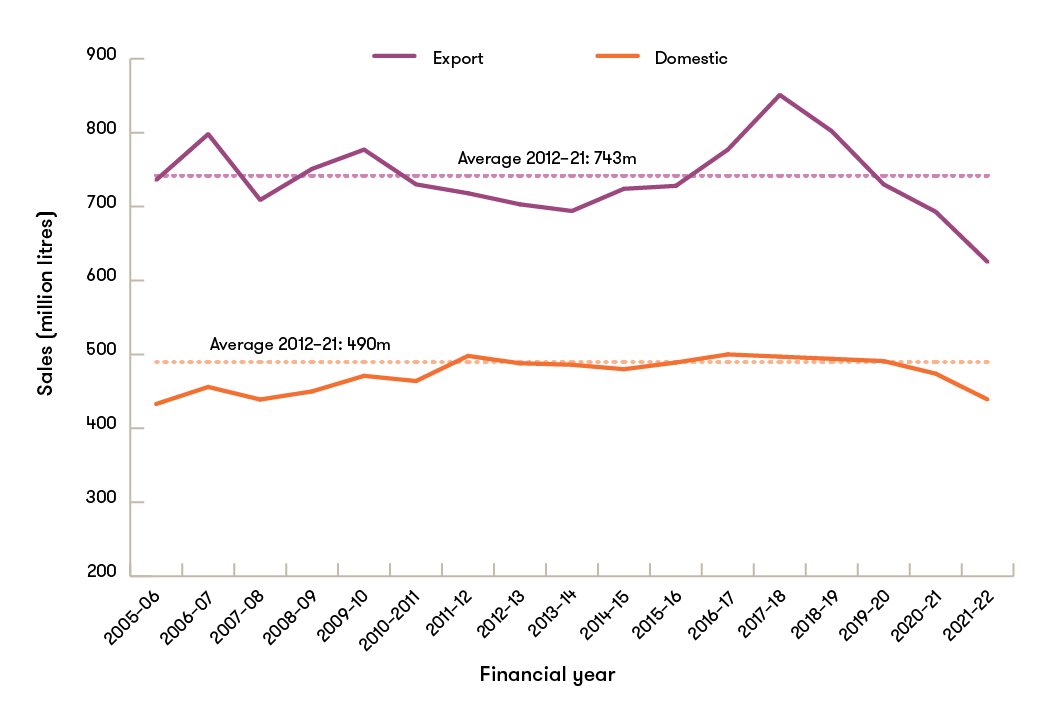

Sales decrease and white increases its share

PSI Survey responses indicate the total sales volume of Australian wine in 2021–22 can be estimated at 1.06 billion litres (118 million 9-litre cases), a reduction of 100 million litres (9 per cent) compared with 2020–21, and 14 per cent below the average for the past 10 years of 1.23 billion litres (Figure 2). Domestic sales are estimated to have made up 41 per cent of total sales – the same as last year –and 4 percentage points higher than in 2017–18, when exports were at their peak.

Domestic sales are projected to have remained generally static for the past 10 years, before starting to decline in 2019–20. Exports have been more variable over time.

Figure 2: Total sales of Australian wine by destination (historical)

The volume of Australian wine exported in 2021–22 was 625 million litres (69 million 9-litre case equivalents), a decrease of 10 per cent compared with 2020–21 and 118 million litres (16 per cent) below the 10-year average of 743 million litres.

Red wine’s share of still wine exports fell from 61 per cent in 2020–21 to 56 per cent in 2021–22, while the white wine share increased correspondingly from 39 per cent to 44 per cent, the highest it has been since 2013–14.

The average value of still red wine exports decreased by 11 per cent in 2021–22 to $4.15 per litre, while the average value of still white wine grew by 5 per cent to $2.15 per litre (Figure 3). Overall, the average value fell from $3.69 per litre to $3.33 per litre FOB.

Figure 3: Australian still wine average FOB value by colour over time

The responses to the PSI Survey indicate that the volume of Australian wine sold domestically in 2021–22 declined by 7 per cent, from an estimated 474 million litres the previous year to 441 million litres (49 million 9-litre cases).

Based on the survey results, the average value of domestic sales is estimated to have increased by 3 per cent to $7.25 per litre in 2021–22. This partly offset the estimated 7 per cent overall decline in sales volume, producing a net decrease of 4 per cent in overall estimated domestic sales value to Australian winemakers, from $3.3 billion in 2020–21 to $3.2 billion. This amount is a mix of wholesale and retail value.

The combined revenue to Australian wine producers from export and domestic sales is estimated to be $5.28 billion, a decrease of 10 per cent compared with the previous year. The decrease reflects the combination of the reduced overall volume and lower average value for export sales.

Rise in inventory driven by red wine

Based on the results of the PSI Survey, the inventory of Australian wine as at 30 June 2022 is estimated to be 2.27 billion litres, an increase of 167 million litres (8 per cent) compared with the same time last year, and 23 per cent above the 10-year average of 1.84 billion litres. Stocks of red wine increased by 16 per cent to 1.44 billion litres. Stocks of white wine decreased by an estimated 2 per cent to 690 million litres.

After being below its long-term average for five years, the national stocks-to-sales ratio (SSR) for reds is estimated to have exceeded 2.0 for the first time in 2020–21 and increased by a further 35 per cent in 2021–22 to 2.77, compared with a 10-year average of 1.64, according to the survey results.

The national stocks-to-sales ratio (SSR) for white wine is estimated to have remained static compared with 2021 at 1.52, which was above the 10-year average of 1.33.

Supply-demand balance has reversed in past two years

Historically, Australian wine supply and demand have been well-balanced. Over the past 16 years, total wine sales have exceeded production in the same year more times than the reverse (Figure 4).

Figure 4: Annual difference between production and sales (historical)

In 2021–22, production is estimated to have exceeded sales. While some of this is necessary to replace stocks drawn down over the previous years, the national inventory is now estimated to be above its long-term average (Figure 5).

Inventory fluctuates during the year, generally being at its maximum just after the new vintage and before any of that vintage has been sold, then depleting over the next 12 months as wine is sold, to be at a minimum just before the next vintage. In 2021–22, the transportation challenges have caused difficulties in getting wine to market, which has a flow on effect in causing wine production capacity constraints for wineries.

Figure 5: Production, sales and inventory of Australian wine (historical)

Outlook

Market conditions continued to be challenging in 2021–22 and producers are likely to face further headwinds in 2022–23, with rising inflation and interest rates having the potential to depress consumer demand as well as increase costs for producers and growers.

A near-average global harvest in 2022 is a small positive for Australian wineries; however, the record New Zealand harvest in 2022 is likely to reduce demand for Australian Sauvignon Blanc on global markets.

Shipping costs have reduced compared with their peak in 2020, and schedule reliability has improved, according to Hillebrand[3].

Another positive for exporters is the decline in the Australian Dollar to US Dollar exchange rate. This has been below US$0.70 since mid-2022 and below US$0.65 since October 2022 (Figure 6).

Figure 6: AUD/USD exchange rate monthly average (2018–2022)

Source: Reserve Bank of Australia

Over the medium term, IWSR forecasts that wine consumption in Australia could fall by a further 10 per cent between 2021 and 2026, while the premium share of the market is expected to increase to 41 per cent by 2026[4]. Similar trends are expected in other mature markets such as the UK and US.

Opportunities for export growth exist, particularly in Southeast Asian markets where wine consumption is growing, and in North American markets, where exports have shown recent growth in both premium and commercial price segments.

Looking ahead to vintage 2023

A third La Niña has dominated weather patterns since winter 2022, causing generally good winter and spring rains, but also record rainfall and flooding in some wine regions. The effect on crop potential is difficult to determine. High rainfall can produce large crops, but crop losses could occur as a result of wet conditions preventing spray applications to manage disease pressure.

Capacity limitations have been reported in large wineries. More than half of the respondents to the PSI Survey 2022 indicated that their estimated available tank capacity for the 2023 intake was less than their 2022 intake. Overall, the total reported available capacity is estimated to be 2 per cent higher than the 2022 vintage but it is unevenly distributed and could limit intake in vintage 2023.

The Production, Sales and Inventory Report 2022 can be found here.

[1] Wine Australia’s Wine Production, Sales and Inventory Survey 2022 (PSI Survey) forms the basis of the results reported here. Wine Australia received responses to the survey from 31 wineries, including 23 of the top 30 by volume, accounting for an estimated 75 per cent of the total grape crush in 2022. While the data accounts for a substantial share of the Australian wine production and sales, it may not be representative of smaller wine business models and is likely to under-state the average sales value for the whole wine sector.

[2] This figure actually refers to wine made from white grapes. The amount of white wine may in fact be slightly higher, as white wine can be made from red grapes – e.g. Pinot Noir for sparkling base.

[3] Hillebrand Trade Dashboard and Oceania Freight Procurement Update September 2022

[4] IWSR 2022