Home to 1.4 billion people and 20 million new legal drinking age consumers each year, India is a market that’s hard to overlook. While the wine market is still small, it holds opportunity for long-term growth. Today’s Market Bulletin will provide an update on the market’s headwinds and potential tailwinds for Australian wine.

A small – but growing – wine market

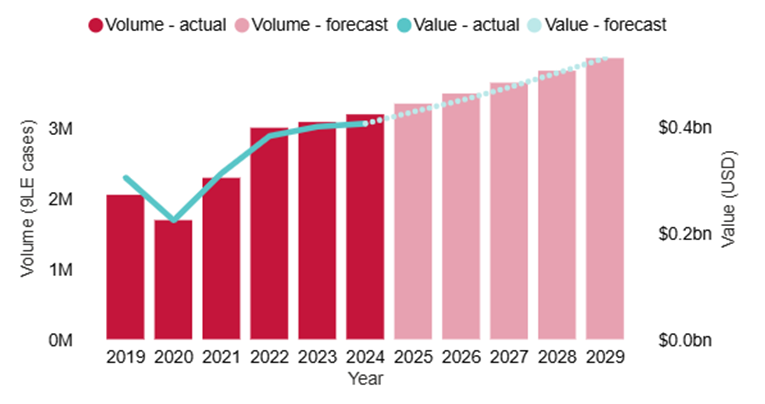

In 2024, wine drinkers in India consumed 3.2 million 9-litre cases of wine, worth US$406 million. While this is only 0.4 per cent of its much bigger total beverage alcohol market (that is dominated by spirits), wine consumption has grown by 9 per cent per year in volume over the past five years and is forecast to grow another 5 per cent per year to 20291. In a world of declining wine consumption, this an attractive prospect. According to IWSR’s India Wine Landscapes 2024 report (summary available here for Australian winegrape levy-payers and exporters) Indian wine consumers show an increasing interest and knowledge of wine, driven by Millennials and Gen X.

Figure 1: Volume and value of wine consumption in India

.png "Fig-1-(1).png")

Source: IWSR data through Wine Australia’s Market Explorer Tool

However, significant challenges in market access remain. Regulations on labelling, distribution and sales of alcohol, and tax structures vary by state (of which there are 28). There are also high tariffs in relation to imported alcohol.

Wine is still a niche category, where distribution networks and underlying infrastructure are still being developed. The Australian Government, as part of “A New Roadmap for Australia's Economic Engagement with India” (February 2025), is working to ease technical and regulatory burdens for Australian wine exporters to India through joint dialogues between the two countries.

While the majority of wine consumed in India is produced domestically, Australia is the number one source of imported wine, with a 42 per cent share of imported wine consumption2. This means that Australia is well-placed to capitalise on market expansion as time goes on.

Trade agreement makes Australia more competitive

Under the Australia–India Economic Cooperation and Trade Agreement (AI–ECTA), which came into force on 29 December 2022:

- tariffs on Australian wine with a cost, insurance and freight (CIF) value of over US$5.00 per 750mL bottle decreased from 150 per cent to 100 per cent upon entry into force, with a further phased reduction of 5 per cent per year for 10 years down to 50 per cent, and

- tariffs on Australian wine with a CIF value of over US$15.00 per 750mL bottle decreased to 75 per cent upon entry into force, with a further phased reduction of 5 per cent per year for 10 years down to 25 per cent.

Figure 2: Phased reduction of tariffs under AI-ECTA

AI–ECTA gave Australian wines above CIF US$5 per bottle a competitive advantage in the Indian market. Depending on exchange rates and shipping costs, a CIF price of US$5 per bottle generally translates to somewhere between A$8 and A$10 per litre free on board (FOB). Exporters can use Wine Australia’s FOB to retail calculator to model the impact of import tariff reductions on retail prices.

Australian wine exports to India are shifting towards higher price points

Australian wine exports to India are on a long-term growth trend, growing by 7 per cent in value per year over the past five years. This growth in value has driven by exports above $10 per litre FOB (see Figure 3).

Figure 3: Value of exports to India by price segment (12 months to December 2025)

Source: Wine Australia’s Export Dashboard

However, 92 per cent of volume shipped to India is still below $7.50 per litre FOB and therefore does not benefit from the AI–ECTA (see Figure 4). Volume below $7.50 per litre has declined by 23 per cent on average per year since 2022, while volume above $7.50 has increased by 14 per cent per year over the same period.

Figure 4: Volume share of exports to India by price segment

EU–India Free Trade Agreement offers potential benefits for Australian wine

On 27 January 2026, the European Union (EU) and India announced the conclusion of their negotiations concerning a free trade agreement that will cut tariffs on EU wine imports. It is expected that tariffs will be reduced in a stepped method, similar to Australia’s under AI–ECTA, and will reportedly lead to rates as low as 20 per cent for premium wines.

While European wines are direct competitors to Australia, there are two ways in which this agreement is positive for Australian wines. One, as wine generally gets cheaper for Indian consumers it will accelerate growth in the wider category, which will ultimately benefit Australian wines as well. Secondly, Australia is afforded a Most Favoured Nation (MFN) condition under AI–ECTA, which means that if other, more beneficial, agreements are subsequently negotiated, Australia will be subject to the same treatment as those countries. In this case, if the tariff rates for EU wines do end up being lower than those Australia negotiated in 2022, Australian wines will likely also be given the more favourable rates.